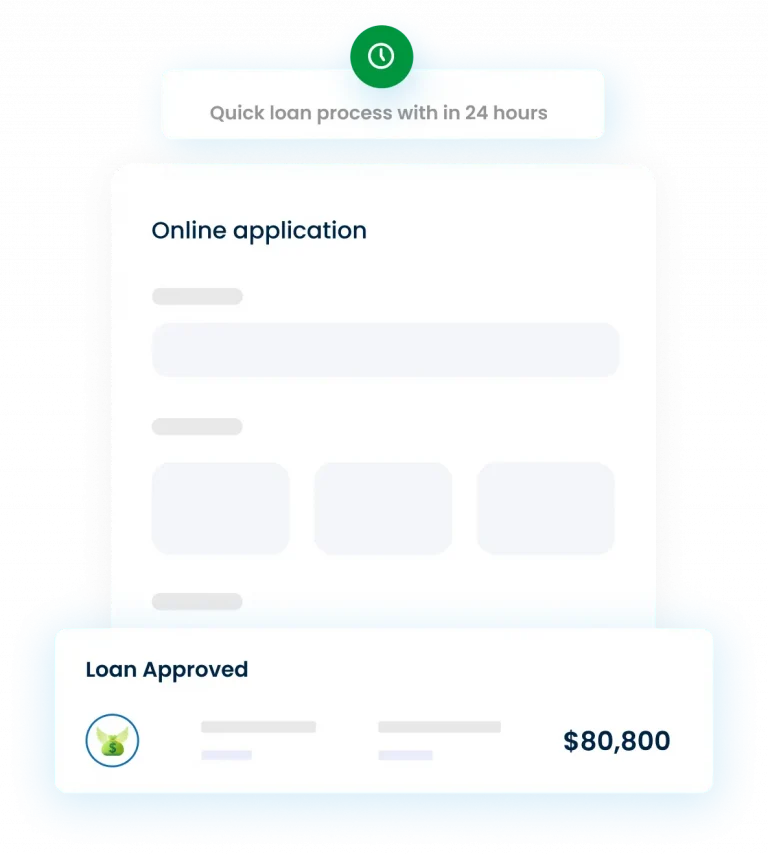

Filling out our secure online application takes just a few moments. Once your information is submitted, we promptly begin searching for a suitable lender or lending partner from our network to assist you. Typically, our clients receive feedback from a lender or lending partner within a few minutes. The final approval and fund disbursement process is expedited, with completion often occurring within 24 to 48 hours.